Happy new year: Welcome to 2020. I rediscovered playing with LEGO Bricks as my kids were growing up. When we attended a Fan Event in 2009, I discovered that being an AFOLwas actually a thing you could do! I now realise that I have been an AFOL for a little over 10 years, and during that time we have seen a number of changes – this coincides with the opportunity to have a look at some of the changes we have seen with the LEGO sets being sold to us over the last decade.

It feels as though the number of sets has ballooned, and that the number of parts in a set has also increased over that time. And what about Licenced themes: Some days it feels as though they have been taking over the LEGO shelves in the toy stores. But have they really proliferated that much?

Now that we are at the end of the 2010’s, I thought we could approach the decade with 2020 hindsight: Let’s take a look at the data in the Brickset Database, and take a year by year look at the number of sets being produced, as well as the number of sets with high part counts (lets define that as over 1000).

We’ll look at the number of themes over this period as well: how many are related to a single intellectual property (IP)? Some themes relate to multiple IPs, while others remain home grown, within the LEGO group, and are dependent on nothing except the imagination of the designers.

Who knows what else we might stumble across along the way. Grab a coffee. There will be graphs. Lots of graphs…

Number of sets released across the 201x’s

I used a query in Brickset to calculate the number of sets released during 2010-2019. I elected to leave our references to technology platforms – Mindstorms, power functions and so forth, as additional elements are also listed in the database, in excess of the number of ‘sets’ for the themes.Collectable minifigurs have multiple entries, so I excluded those at the expense of duplicates. I removed Technic and Duplo from this data, as they are both aimed at fairly different markets to the bulk of the system offerings. I shall consider them both independently. The main drawback of this entire methodology is that it considers sets RELEASED this year, but has no relation to the number of sets still available, either in real life or online stores.

As you can see, there was steady growth in the early part of the decade, until 2016, when the number of sets released was fairly steady. In 2019, we saw a drop off in the number of sets released by approximately 10%. This might be part of the decision in 2018 to institute some fiscal restraint, to reduce new sets and assembly line configurations; reduce the number of creatives in the organisation, or perhaps to increase the focus on the number of larger sets, at higher price points. I shall come to that later.

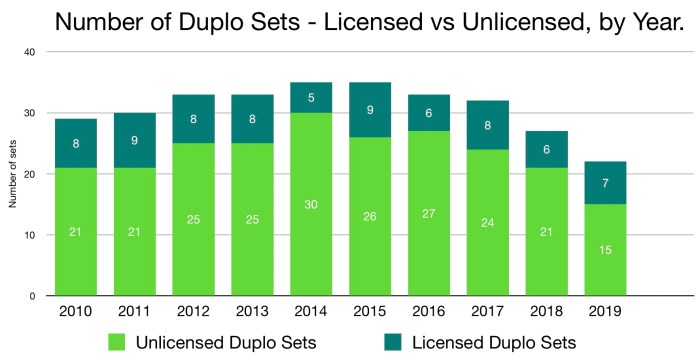

Number of Duplo Sets

Duplo, the preschool range, celebrated its 50th anniversary this year. Early childhood learning is really important for a child’s later growth and development. I felt some what despondent when I looked at the next graph: number of Duplo sets released by year. As you can see, there has been a stead decline in the number of DUPLO Sets released during the last four years: by more than a third!

Around 2014, however, LEGO released a new theme: Juniors. This theme included content from both in-house material such as LEGO City, Friends and Ninjago, and salso external IPs such as DC and Marvel superheroes, and Disney Princess, and Jurassic World. these sets featured simple construction and no stickers. The final releases for this range occurred in 2018, with a new 4+ label appearing with the core themes in 2019. This year’s sets also included several Star Wars sets, as well as the Toy Story 4 theme. I added the Junior and 4+ sets to the Duplo release graph:

There is no definite trend or correlation in the total set numbers between 2014 and 2017 – with 43-50 sets released each year during this period. In 2019, there is a reduction in the total number of sets released for younger builders, in keeping with what is observed through most of the other themes.

Number of Technic sets

I also extracted the number of LEGO Technic Sets from the database for the last 10 years, and saw that there appeared to be an increase in the overall number of Technnic sets released in the last few years. In part, this would be in keeping with the success of the Porsche and Bugatti models, truly epic builds for any person keen on LEGO Technic construction.

Increasing from an average of 10 per year to 13-14 in the last couple of years seems to be a legitimate trend. Technic sets tend to be aimed at an older age group than other sets. The cynic in me might suggest that this has been a deliberate ploy to tempt mechanism enthusiasts to buy more sets…

Licensed themes: Coming or Going?

Now, what about licensed themes? Some seem to come and gone, before you blink – examples from the last decade might include Prince of Persia and the Lone Ranger. Some that have shown a bit more longevity include Harry Potter and Lord of the Rings, but certainly Star Wars has been the most consistent over the years, as far as regular releases. DC and Marvel super heroes have also become a regular fixture amongst the licensed releases.

We know that, to an extent, licensed themes have become a important way for LEGO to market sets – the familiar characters offer an easy gateway into story telling with a set – reliving the adventures from the Comic/Book/Tv series/ movie, or in more recent times Video Game, with Minecraft and Overwatch now part of the mix. Technically, Architecture sets might require licensing from local authorities to develop sets based on local landmarks, so, for the purpose of this exercise, I am considering architecture to be a licences theme. The LEGO Movies – including Batman and Ninjago, as well as TLM1&2 are, technically, external IP’s, controlled by Warner Brothers.

I had a look at the relative number of themes that were present from 2010 to 2019, and classes them as an external licence, an In house IP pr a theme using IP from multiple sources.

External, 3rd party themes are typically obvious and include those such as Star Wars, Disney or DC Superheroes.

In house themes: those that were developed within the LEGO Group. Sometimes they are developed in conjunction with Cartoon Network, such as Mixels, Ninjago or NEXO Knights; and others just exist in their own way, such as friends and LEGO City (although the accompanying animated series is now a regular feature of some of these themes).

Then there are themes that might feature models from different IPs – both those that are developed in house and also using external IPs – such as Creator Expert. Others might use multiple IPs in a given year – Speed Champions and Brickheadz are probably the most obvious at present. The sets that went with LEGO Dimensions might be considered in a similar way. Some themes, such as collectable minifigures, started life as an in-house theme, for a couple of years, but in recent times have incorporated up to three IPs in a given year.

I have not included LEGO Ideas in the mix for this one: over the years, there have been a mixture of Original themes, Licenced vehicles (Curiosity rover; Saturn V) and Media related sets: Minecraft, Doctor Who, Wall-E, Voltron, Steamboat Willie and most recently, Friends).

There is a definite trend for an increase in themes containing external IP. Lets make it clear by merging both categories that relate to external IP’s.

In recent years, we have seen fewer and fewer in-house themes, and an increase in external IPs chosen as a subject for set design. As someone who still feels nostalgic for Town, Castle and Classic Space, seeing themes like Pirates supplanted by Pirates of the Caribbean in recent years is a bit disappointing. Many of todays 20, 30,40 and 50 year olds grew up on in house themes such as Aquanauts, Alpha squad, Pirates, Blacktron, Space police (I II and III), Power miners, Atlantis and so forth, but we are now seeing these in house themes waning in there popularity. The recent arrival of Hidden side is breathing a new life into the in-house themes, with excellent back story, quality set design and incorporation of an augmented reality app (for the young people to play with.) Indeed, this trend is common in the cinema multiplexes as well these days, with many movies being released as part of ongoing franchises now a regular feature in the summer release schedule.

Of course, kids have their favourites too, and Duplo has its own range of licensed themes, predominantly Disney based at present, but previously other themes, including Bob the Builder. Interestingly, the number of licensed sets in Duplo is lower than it was 5 years ago…

As for Technic, If you love a certain car or Truck, chances are at some stage, Technic will produce a licenced version of it. In fact, there are more Licensed Technic sets being produced each year now, compared with 10 years ago. In part, this accounts for the increase in the number of Technic sets being produced Annually.

The Mouse in the Room

And how does Disney fit into the mix, as far as licenses are concerned? Disney licenses are a safe bet for marketing as far as LEGO are concerned, and we have seen some interesting sets emerge over the years through films such as Prince of Persia, and even the Pirates of the Caribbean franchise. Prince of Persia in particular introduced wider use of some interesting architectural elements, as well as increased use of Dark tan. I have looked at all licensed sets as tagged in the Brickset database, and used that to determine number of licensed sets. Brickheadz were counted manually: they are all considered licensed by Brickset; Ideas, Juniors and Creator Expert were also added in this way. I also added in CMF series – Just as 1 set per series.

Lucasfilm was sold to Disney in 2012, so I have only considered LEGO Star Wars sets as Disney since 2013; Likewise the Marvel sets relating to non-Marvel Studios properties – comics, X-men and non-MCU Spiderman have been excluded from the Disney count. Hopefully this is a correct interpretation.

Disney themes included: Disney Marvel Superheroes (partial); Prince of Persia, Princess, Frozen, ‘Park sets’, 2 series of CMF, The Lone Ranger, Cars, Toy Story, The Incredibles and Star Wars (after 2012).

There were no ‘permanent’ Disney licenses in 2010-2012: the first wave of Toy story, and Prince of Persia account for most of the licensed sets that year. Star Wars entered the range in 2013, while the Disney Princess sets first appeared in 2014. The Marvel Cinematic universe made their first forays into LEGO in 2012, and have been a significant presence for the last few years. For actual numbers, Star Wars was generating around 20-26 sets before the acquisition, 33 per year before the release of Force Awakens, and consistently over 40 since: which is not too surprising considering the resurgence of interest in the franchise, as well as the increase in new source material to draw from each year.

Looking at the relative proportion of LEGO Star Wars, to total sets produced, the proportion has been relatively unchanged.

As you can see, Licensed sets are now approximately 50% of the LEGO portfolio (not looking at Technic or Duplo). We saw an incremental increase in 2014, with the appearance of the LEGO Movie sets. In 2017, the release of Brickheadz also increased the number of licensed sets, Disney and otherwise, but these only account for around 20 – 30 sets in those 2 years, and only one in 2019.

Price analysis

Is LEGO getting cheaper to buy? Or is it getting harder to find a set that your child can buy with their own pocket money? In real life, if we are not buying individual elements from Bricklink, BrickOwl, or that bloke down at the market, we are likely to purchase LEGO as a set. Most likely with a model to build. Looking at models now compared with way back when I was a lad is like comparing 8 bit, blocky graphics with UHD 4K: more smaller elements, more curves and more colours. The level of detail that can be resolved on a contemporary set, compared with those from the past is significantly greater.

So, have there been any shifts in the pattern of pricing over the last decade? I have chosen to refer to the Brickset data on price in GBP at the LEGO store as a gauge to the price: it tracks better with Europe than USD prices, which were given a correction earlier in the decade Anyway… I chose GBP over Euro because there were some holes in the data when I was querying the database late at night. (I concede some of the problems might have existed between the Keyboard and the Chair.)

I selected several price bands, and then further simplified them after initially looking at the data:

The simple, obvious message here is that there are virtually no sets available for less than £5 anymore. Please remember, this data does NOT include Collectable Minifigures. There are definitely more sets costing £150. Around half of these sets are over £200. But, because of the rise and fall in the number of sets being produced, lets normalise that data – so each band is represented as a percentage of the sets available for sale each year. If the relative numbers of sets at a given price band is consistent as a percentage, the number in that band won’t change.

The number of sets under £5 has virtually vanished, the proportion of sets costing £5-£19.99 has also decreased, with slight, but consistent increases in the the number of sets in the more expensive brackets. There is a definite increase in the proportion of expensive sets on the market, relative to the total number, even in 2019, when there was a drop in the total number of sets produced, with 20% costing over £60 and 8% over £100. In part, I am sure some of this rise can be attributed to licensing fees associated with external IPs, but also with an increase in sets with a large part count, and directed towards the adult market (of course, these sets are more likely to be based on an external IP).

Part count

With this relative increase in set numbers, and prices, have we seen an increase in the proportion of sets with part counts over 1000 elements?

With the Creator Expert sets, we have always had a few sets with parts counts over 2000 on the books, but we have seen an increase in sets in the 1000-1500, and 1500-2000 element brackets. Sets with more than 3000 elements are now becoming part of the annual release cycle since 2017. The proportion of the Total number of sets with part counts over 1000 has increased from 4.5% in 2010 to a little over 8% in 2019: from 10 to 32 sets!

Of the 68 sets with more than 2000 elements, 28 (41%) are from IPs developed in house.

Given the trend we have seen here, I was wondering if there was a decrease in smaller part count sets overall. Given the changes in absolute part count, I also normalised this data as a proportion of number of sets released:

So here we see a decrease in the absolute number of sets with fewer than 500 elements, and also a decrease in the proportion of sets with a a lower part count. We also see a significant increase in the number of sets with more than 1000 elements in 2019.

Technic part counts.

And has this trend been followed in Technic?

The first Technic set with more than 2000 elements was the 8110 Unimog from 2011. There has been an increase in the number of higher price counts in the last 5 years, and in that time, and many of those have been attached to a 3rd party license.

Recommended ages:

The past year has seen an interesting change in the labelling of many sets: compared with previous years, the number of sets with no upper age limit has increased, by a factor of 3. In the past this has been used as an indication of a broad range of appeal that a set might have for a given stage of development. However, with the broad appeal of some licenses, removing this upper limit acts as a way of giving consumers permission to buy a set, knowing that it is still age appropriate. As such, many more sets have been labelled (age)+

This looks quite cluttered, so let’s just look at the top end of these sets – say 10+:

We see an significant increase in sets aimed at 10 years and over in 2017: in part, this coincides with the wider release of the Brickheadz. This increased again in 2018, and dramatically reduced in release number in 2019. There is a significant increase in the number of sets aimed at over 16’s. Some of these are the Architecture sets (Trafalgar Square and Empire State Building): this also the case for the 2020 Skyline releases. Many of these were previously labelled 12+. the top bracket also includes most of the Creator Expert sets, with the exception of the Winter Village sets, which tend to be targeted a little lower. This would be consistent with the increased number of sets with higher part counts, as well as more expensive sets, as a total proportion of sets in the portfolio.

In Conclusion, Let’s Apply 2020 Hindsight…

In summary, during the period 2010-2019, we have seen a significant increase in the number of LEGO sets released each year. There has been a tendency for sets to be more expensive, with large sets (high part counts, expensive, and aimed at older consumers – over 10 years of age) increasing both in absolute number, as well as a proportion of the total LEGO releases for the year. This is in the face of a 10% reduction in the number of sets released in 2019, compared with the previous years.

We have seen an increase in the number of External IPs (licensed themes) being used, and a reduction in the number of in-house themes. There has been a reduction in the absolute number of DUPLO sets being released each year, offset in part by the Juniors and 4+ sets.

There has been a tendency for Technic sets to get larger, over the years, and there has been a slight increase in the number of Technic sets released each year.

LEGO Star Wars celebrated its 20th anniversary this year. We saw a surge in sets associated with the release of the Force Awakens, and the number of sets produced has been fairly consistent since then, and been fairly consistent at 10-12% of the total number of LEGO sets released each year, both before and after the acquisition of Lucasfilm by Disney.

The proportion of Licensed sets has doubled during the course of the decade, from 25% in 2010 to around 50% in 2019. We saw a significant increase in 2014, when Disney Princess sets started to roll out, as well as sets, in preparation for the LEGO Movie in 2015.

I have been engaged with LEGO as a product for about 15 years, initially with my children, before starting to discover the world of the AFOL communities in 2009. Subsequently, as I have engaged more and more with the product, There has been a feeling of “More licensed sets”, “More expensive sets” “Lots of Disney” and maybe, more sets of appeal to the wider community.

If LEGO is to survive as a company, it needs to expand its target demographic beyond children, and adult fans, and continue to produce sets of interest to the wider community. The Chinese New Year sets have been a great example of this, as have the Creator Expert Vehicle sets. Architecture appeals to many adults, evoking memories and dreams of travel, or of past homes. Television and Movie franchises appear to all ages, and there is no doubt that these appeal a lot to adults – brought to LEGO through their love of a particular movie or TV program. The recently released Ideas set, based on Central Perk, from the sitcom Friends is a great example of this, with stock vanishing from the shelves as fast as it can arrive.

Concern was expressed a couple of years ago when it was announced that LEGO was going to be cutting costs: resulting in staff redundancies, as well as other measures to improve the bottom line. Since then, while we have seen a drop in the total sets produced in 2019, we have also seen an increase in larger sets, more expensive sets, and there are more sets aimed specifically at adult audiences. Ten years ago, AFOLs were not considered to be an overly significant part of the group’s bottom line: close to 5% was the number quoted around that time. (But was that purchases? Purchasers? Revenue? Profit? All numbers can be a bit rubbery.) I wonder what proportion of revenue might now be considered to be the result of Adult fans? Certainly there are more products being aimed at this market now, compared to ever before.

The recent purchase of secondary marketplace, Bricklink, by the LEGO Group suggests an ongoing active interest in engaging with AFOLs, and understanding what they might be looking for – although recent changes to the terms and conditions for using Bricklink – removing all customised, modified and third party elements from the platform, as well as any MOCs for sale involving 3rd party IP, leaving many in the AFOL community with concerns about future directions here.

What is the best balance in the long term for Adult and child oriented sets, licensed and in-house themes within the LEGO range? I have always found a lot of appeal in the in house themes produced by LEGO. In recent years, themes such as Friends and Elves, Ninjago, Legends of Chima and now even LEGO City have been associated with a television series to drive awareness and sales. We have lost many of those in-house action themes, which used to be so prevalent: Power Miners, Atlantis, Monster Fighters. Castle seems to have become Harry Potter (and previously Lord of the Rings); Space has become Star Wars. The sets, and the story telling, feel as though they have been outsourced in recent years, although with Hidden side, perhaps we are seeing a return. It will be interesting to see how the theme endures into the future. Interestingly, in the absence of some of these themes, we are seeing LEGO City step up too the plate, with ‘real world’ adventures springing up on a regular basis: Volcano Explorers, jungle Explorers, Arctic, deep sea, and in 2019, the Mission to Mars! LEGO City is approaching its 15th anniversary: perhaps it might be time to visit the shifting empress of this theme. But not today. This post has got on long enough.

The 2010’s have been kind to AFOLs, and we continue to be offered sets that appeal to many, more often than not! What do you feel about the direction that has been taken? How do you feel about the prevalence of Licensed sets available today? the rising part count? the changes in design aesthetic?

Why not leave your comments below, share this post with your communities, and until next time, have a Happy New year and…

Play Well!

While you are here….

You have probably heard about the current Bushfire Emergency, engulfing the eastern states of Australia.

Jay, over at Jay’s Brick Blog is running a fundraiser, with proceeds going to the Red Cross, to help with relief efforts. You can read about it, and make a donation, here: https://jaysbrickblog.com/2020/01/03/raising-funds-for-the-australian-bushfire-crisis/

Great read, loved the graphs as the visual helps understand your point. 😊

Thanks Steve.

Great post with lots of interesting analysis. Happy new year!

Happy new year to you too.

Lots of detail here! Now I want to see the same type of analysis, but for the 2000s.

[…] my review of the decade revealed a number of trends, including the increased marketing of large, licenced sets, to adult […]

[…] Supercars of all sorts have always been a part of the Technic lineup, ever since 1978. To be basing a LEGO set on a car featured in this popular movie franchise looks like it will pick up a lot of fans around the world (not so much LEGO Fans, although they will pick it up, as car fans, returning to LEGO. An adult marketed set, featuring advance building techniques, over 1000 elements, and based on a licensed theme…I’m not too surprised – this has been a trend for the last few years, […]

[…] so such sets have a place today? In our recent survey of the sets released in the 2010’s, we have seen a reduction in the overall range of DUPLO sets, aimed at the […]

[…] this is no big surprise: in our review of the decade, we saw that there are more and more LEGO sets aimed at adults: complex building; luxury branding; […]